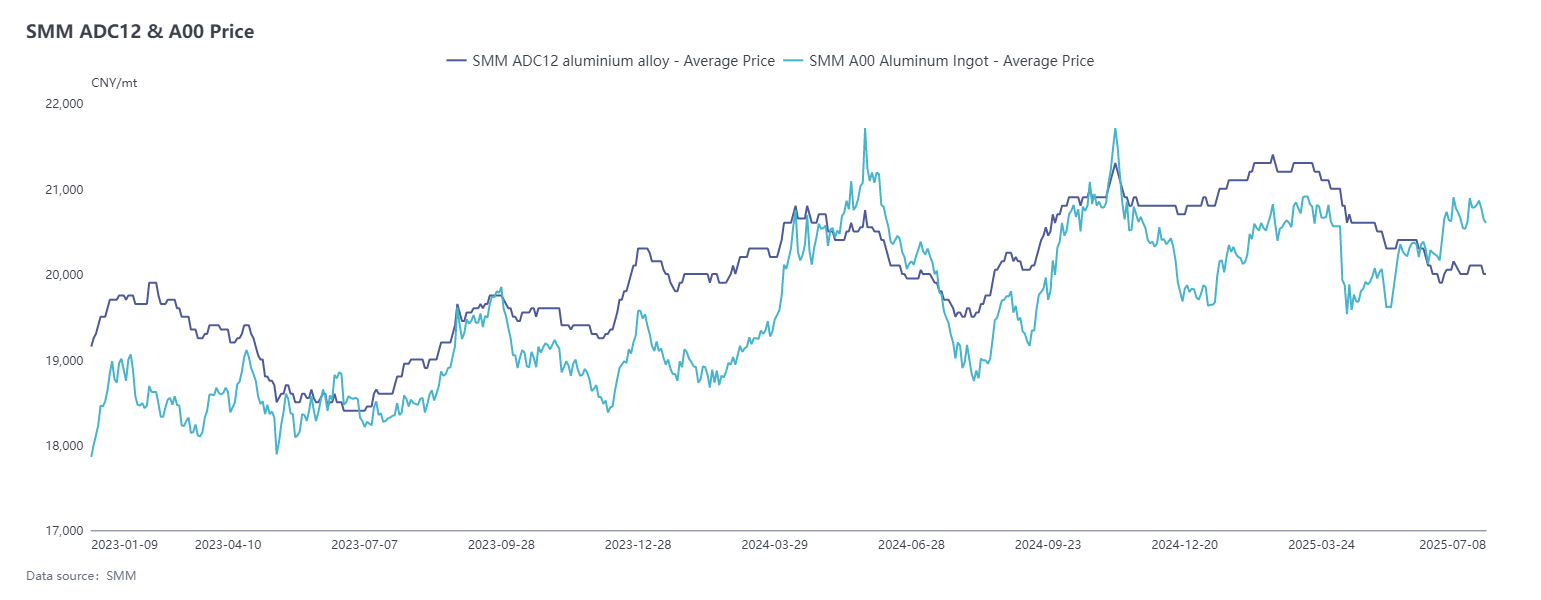

In terms of aluminum prices, the price center continued to move upward in June. As of June 30, the most-traded SHFE aluminum 2508 contract closed at 20,580 yuan/mt. In the spot market, the SMM A00 aluminum ingot prices rose by 490 yuan/mt from the previous month-end to 20,780 yuan/mt on June 30. The average spot aluminum prices in June (calendar month) reached 20,535 yuan/mt, up 2.0% MoM.

Regarding secondary aluminum alloy prices, on June 10, cast aluminum alloy futures officially commenced trading on the SHFE. Driven by the need to narrow the spot-futures price spread, as the listing benchmark price of 18,365 yuan/mt was significantly lower than the spot price, the main continuous futures contract surged strongly to around 19,500 yuan/mt upon opening. Subsequently, the futures market generally followed the fluctuations of SHFE aluminum. As of July 7, the most-traded cast aluminum alloy 2511 contract closed at 19,750 yuan/mt. However, the spot price growth was sluggish, with the SMM ADC12 price remaining stable at 20,000 yuan/mt on July 7 compared to the beginning of the previous month, and the theoretical premium against the most-traded contract narrowed from 685 yuan/mt on the first day of listing to around 260 yuan/mt.

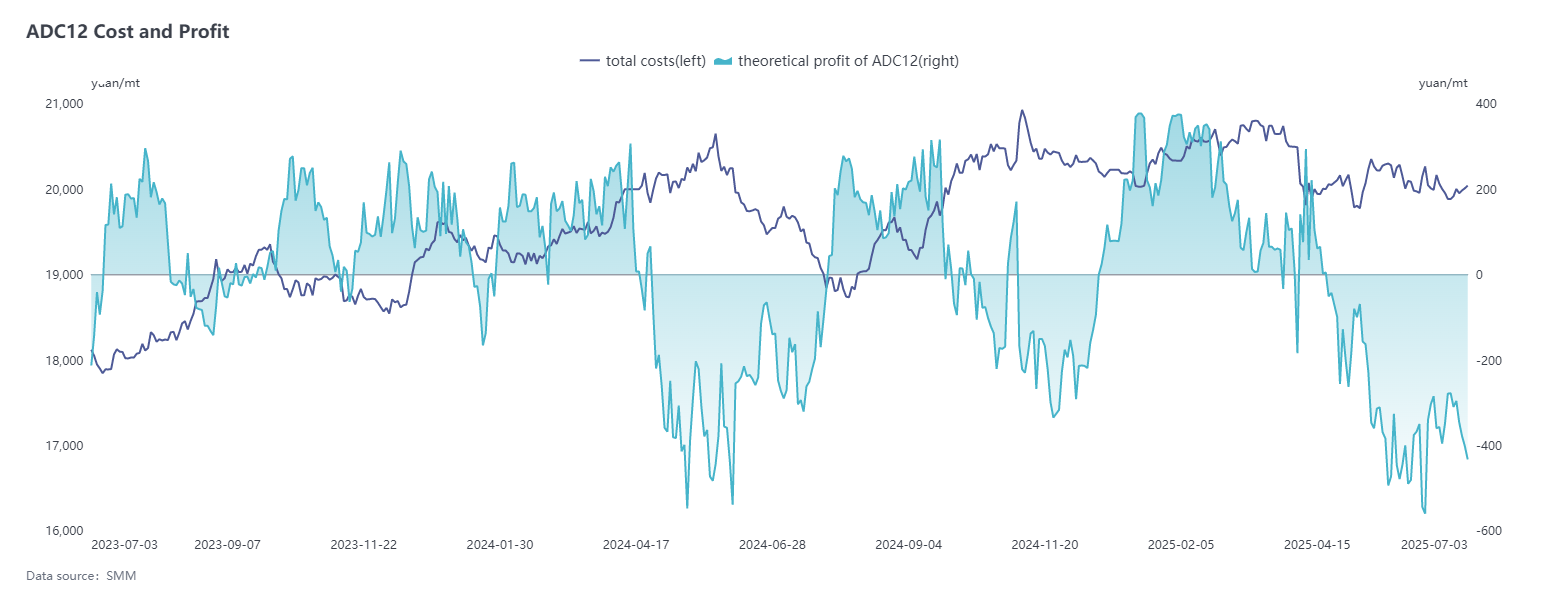

On the cost side, aluminum scrap prices rose in June along with domestic aluminum prices. Coupled with the upward trend in the prices of core raw materials such as silicon (oxygen-blown #553 silicon prices rose 600 yuan/mt MoM to 8,750 yuan/mt) and copper, the cost of ADC12 was significantly pushed up. However, it was difficult to effectively pass on the cost pressure to the product selling price. Meanwhile, the tightening of raw material circulation increased the difficulty of procurement for enterprises, leading to a week-by-week increase in cost pressure and a continuous expansion of the theoretical loss ratio in the industry.

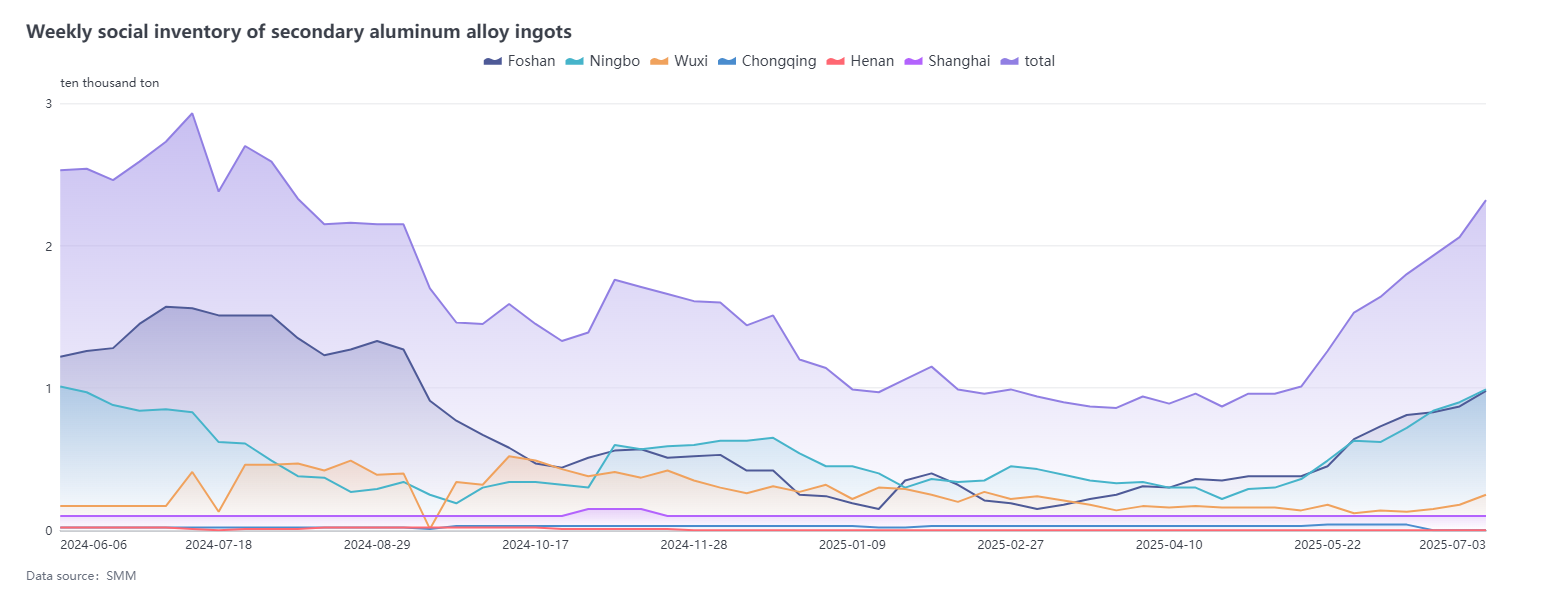

Demand side, in June, orders related to new energy showed moderate performance, and the easing of tariff impacts drove a recovery in growth for some downstream orders. However, overall consumption remained weak, and high aluminum prices continued to suppress downstream purchase willingness. Although the listing of futures increased the inquiries for delivery brands among futures-to-spot traders, actual consumption support remained insufficient, and ADC12 prices lacked upward momentum. Additionally, social inventory continued to accumulate. According to SMM statistics, the social inventory of secondary aluminum alloy has seen inventory buildup for eight consecutive weeks, increasing by 6,866 mt to 23,232 mt MoM in early July. Against the backdrop of inventory at high levels, low-priced supplies flooded the market, further intensifying competitive pressure and keeping ADC12 prices under sustained pressure.

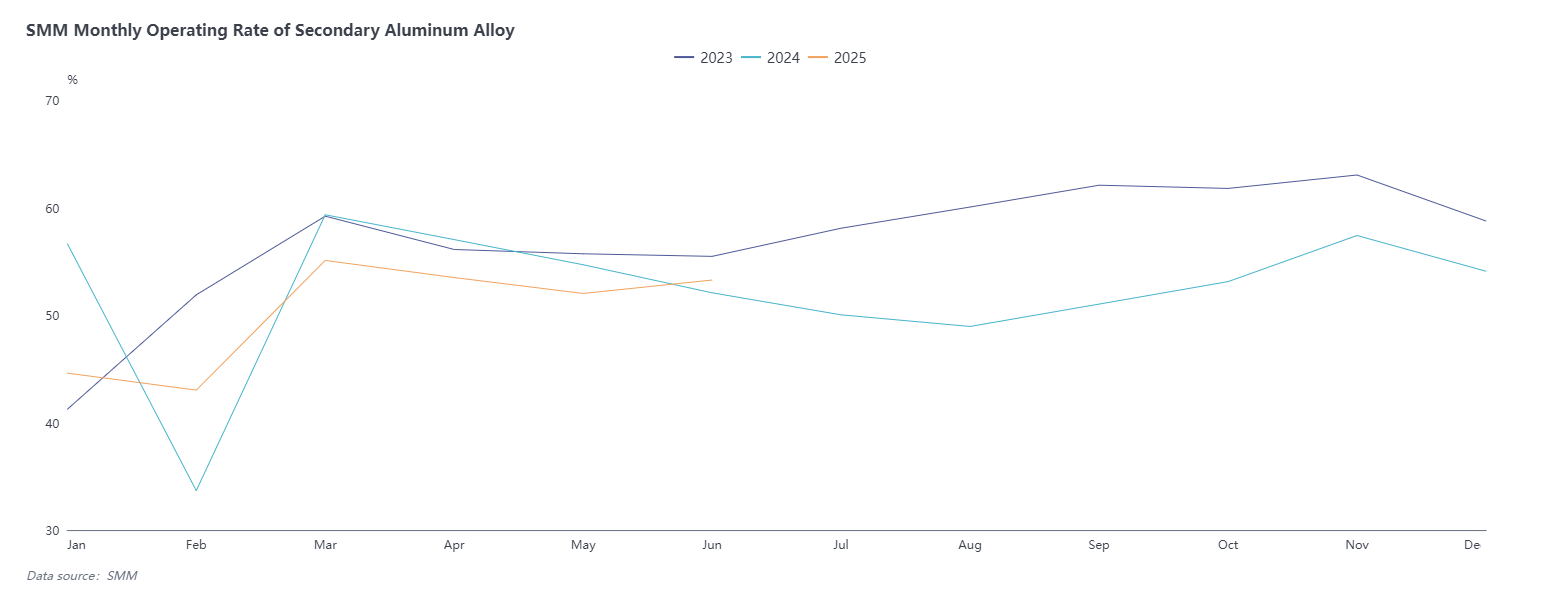

In terms of supply, the operating rate of the secondary aluminum alloy industry in June increased slightly by 1.25 percentage points MoM to 53.26%, and rose by 1.20% YoY. The growth was mainly attributed to two factors: firstly, the increase in orders from the NEV sector drove the operating rate of some large plants, which primarily use aluminum liquid, to exceed expectations; secondly, compared to May, there were no holiday disruptions in June, leading to a recovery in production. Entering July, the trend in the operating rate of secondary aluminum producers continued to diverge. Large plants, leveraging their stable orders and the advantage of delivery brands, are expected to increase production, driven by the active procurement of ADC12 by futures-cash arbitrage traders. However, the traditional off-season effect continues to manifest, with automakers potentially cutting production plans due to factors such as high-temperature holiday arrangements and finished product inventory backlogs. Additionally, with the tightening of raw material circulation and worsening cost losses, some enterprises have already initiated furnace shutdowns for maintenance at the end of June or the beginning of July, which will drag down the overall operating rate of the industry. Based on a comprehensive assessment, the operating rate of the secondary aluminum alloy industry in July is expected to decline slightly while remaining stable.

In July, the tight supply of secondary aluminum raw materials is expected to persist due to reduced aluminum scrap imports and lower dismantling volumes caused by high temperatures, which will continue to support ADC12 costs. The increasing difficulty in sourcing materials may further strengthen this support. Demand side, although market expectations for H2 consumption have turned optimistic, in the short term, the deepening off-season in July amid high temperatures will continue to suppress the operating rates of downstream die-casting enterprises. Coupled with high aluminum prices weakening end-user order purchase willingness, the sluggish demand is unlikely to improve, forming the core resistance to ADC12 price increases. Overall, strong cost support and weak demand suppression will continue to compete, with ADC12 prices expected to fluctuate rangebound in a weak pattern in July.

In the futures market, the cast aluminum alloy futures are currently in their early listing phase, with the most-traded contract being the distant-month 2511 contract, and market sentiment remains cautious. Current participants are mainly producers, futures-spot traders, and merchants, with limited engagement from downstream enterprises. The futures market has not yet impacted spot prices or altered the existing pricing system. In the short term, cast aluminum alloy futures are likely to continue following SHFE aluminum trends.

Recently, close attention should be paid to raw material circulation and demand-side fluctuations, while continuously monitoring the spillover effects of improved futures market liquidity on the spot market.